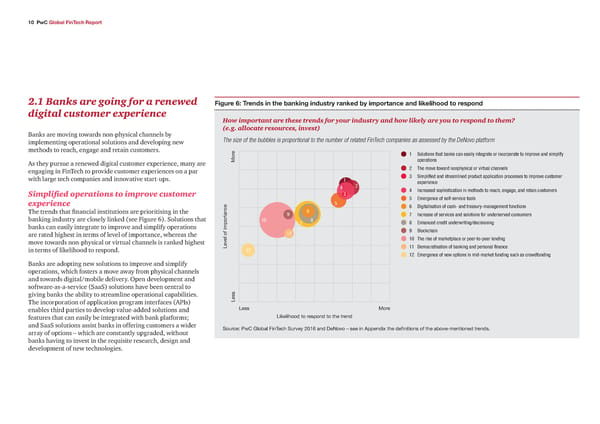

10 PwC Global FinTech Report 2.1 Banks are going for a renewed Figure 6: Tren s in the baning in ustr rane b importance an lielihoo to respon digital customer experience How important are these trends for your industry and how likely are you to respond to them? (e.g. allocate resources, invest) Banks are moving towards non-physical channels by The size of the bubbles is proportional to the number of related FinTech companies as assessed by the DeNovo platform implementing operational solutions and developing new methods to reach, engage and retain customers. e 1 Solutions that banks can easily integrate or incorporate to improve and simplify As they pursue a renewed digital customer experience, many are ‘or operations engaging in FinTech to provide customer experiences on a par 2 The move toward nonphysical or virtual channels with large tech companies and innovative start-ups. 1 Simplified and streamlined product application processes to improve customer 2 eperience Increased sophistication in methods to reach engage and retain customers Simplified operations to improve customer mergence of selfservice tools experience € ‚igitalisation of cash and treasurymanagement functions The trends that financial institutions are prioritising in the † € ƒ Increase of services and solutions for underserved consumers banking industry are closely linked (see Figure 6). Solutions that 1ˆ ƒ „ „ nhanced credit underwriting…decisioning banks can easily integrate to improve and simplify operations importance † ‡lockchain of 11 are rated highest in terms of level of importance, whereas the 1ˆ The rise of marketplace or peertopeer lending move towards non-physical or virtual channels is ranked highest “e€e 11 ‚emocratisation of banking and personal finance in terms of likelihood to respond. 12 12 mergence of new options in midmarket funding such as crowdfunding Banks are adopting new solutions to improve and simplify operations, which fosters a move away from physical channels and towards digital/mobile delivery. Open development and software-as-a-service (SaaS) solutions have been central to giving banks the ability to streamline operational capabilities. The incorporation of application program interfaces (APIs) “ess enables third parties to develop value-added solutions and “ess ‘ore features that can easily be integrated with bank platforms; “iˆeihood to respond to the trend and SaaS solutions assist banks in offering customers a wider Source: ‚ƒ …oa FinTech Sur€ey 21† and eo€o – see in Appendi the definitions of the ao€e™mentioned trends„ array of options – which are constantly upgraded, without banks having to invest in the requisite research, design and development of new technologies.

Global FinTech Report Page 16 Page 18

Global FinTech Report Page 16 Page 18